The Crucial Role of Financial Representatives in Retirement

Posted by Ethan Ball, IAR

Serving Cedar Rapids, Iowa, and Surrounding Areas.

Comprehensive Tax and Investment Strategies for High-Income Earners in 2024

When you’re a high-income earner, managing your finances isn’t just about making money—it’s about keeping as much of it as possible. To do that, you need a solid game plan that focuses on optimizing your taxes and growing your investments. Let’s break down some of the best strategies for 2024 to help you stay ahead.

1. Max Out Your Pre-Tax 401(k)

One of the simplest yet most effective ways to lower your taxable income is by contributing to your 401(k). In 2024, you can put away up to $23,000 into your 401(k), and that includes both traditional and Roth 401(k) accounts. Here’s the kicker: your employer’s matching contributions don’t count toward this limit, which means you could potentially see a total contribution of up to $66,000 when you factor in your employer’s match.

- Traditional 401(k): Contributions are made pre-tax, which can be a big help if you expect to be in a lower tax bracket during retirement.

- Roth 401(k): You pay taxes on your contributions now, but all your withdrawals (including earnings) are tax-free when you retire.

Strategy Tip: Always contribute enough to get the full employer match—it’s essentially free money!

2. The Mega-Backdoor Roth

If you’ve maxed out your 401(k) but still want to save more, the mega-backdoor Roth strategy could be your ticket. This involves making after-tax contributions beyond the $23,000 limit, up to the overall cap of $66,000. Then, you can roll these extra contributions into a Roth IRA or Roth 401(k), giving your retirement savings a significant tax-free boost.

Keep in Mind: Not all 401(k) plans allow for after-tax contributions or in-service withdrawals, so check with your plan administrator first. And because this strategy can get complicated, it’s worth consulting with a financial planner.

3. Individual Retirement Accounts (IRAs)

When it comes to IRAs, the Roth IRA often steals the spotlight. In 2024, you can contribute $6,500 per year, with an extra $1,000 if you’re 50 or older. If your income is too high to contribute directly to a Roth IRA, don’t worry—you can still use a backdoor Roth IRA strategy. Just be careful if you have other pre-tax IRA funds, as the pro-rata rule might make some of your conversion taxable.

- Traditional IRA: Contributions might not be deductible if you’re covered by a workplace plan and your income is over a certain threshold.

Strategy Tip: The backdoor Roth IRA is a powerful way to build tax-free retirement savings, even if you’re above the income limits for direct contributions.

4. Utilize Other Pre-Tax Options

HSAs and FSAs aren’t just for healthcare expenses—they can also be fantastic tax-saving tools.

- Health Savings Account (HSA): For 2024, you can contribute up to $8,300 for family coverage or $4,150 for individual coverage, with an extra $1,000 catch-up contribution if you’re 55 or older. The best part? Contributions are tax-deductible, and both growth and withdrawals for qualified medical expenses are tax-free.

- Flexible Spending Account (FSA): In 2024, you can contribute up to $3,250. Just remember, you’ll need to use the funds within the plan year, though some plans offer a small rollover.

- Dependent Care FSA: Save up to $5,000 pre-tax for childcare expenses.

Strategy Tip: HSAs offer triple-tax benefits—tax-deductible contributions, tax-free growth, and tax-free withdrawals. If you’re eligible, max out those contributions and invest the funds for the long term.

5. Donate to Charity

Giving back can be a win-win for you and the organizations you support.

- Cash Donations: Deduct up to 60% of your adjusted gross income (AGI) in 2024.

- Appreciated Securities: Donate these directly to avoid capital gains taxes on the appreciation, while still getting a deduction for the full market value.

Strategy Tip: Consider bunching your charitable donations into one year to exceed the standard deduction and maximize your itemized deductions.

6. Invest in Real Estate

Real estate can offer some incredible tax benefits, like depreciation and the ability to defer taxes on gains through 1031 exchanges. If you qualify as a real estate professional, you can even use rental real estate losses to offset other active income.

- Qualified Opportunity Zones: Invest here, and you can defer taxes on capital gains until 2026, with potential tax-free growth if you hold the investment for at least 10 years.

Strategy Tip: Real estate investments can be a great way to reduce your tax burden, but they require careful planning. Be sure to consult with a tax advisor.

7. Roth Conversions

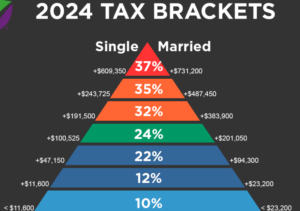

Consider doing Roth conversions during years when your income is lower or during market downturns to convert pre-tax assets at a lower tax rate. While there’s no limit on how much you can convert, remember that the converted amount will be added to your taxable income for that year.

Strategy Tip: Keep an eye on your tax bracket to make the most of this strategy.

8. Manage Your Equity Compensation

Equity compensation can be a significant part of your income, but it comes with its own set of tax implications. Whether you have RSUs, NSOs, ISOs, or ESPP shares, the key is to understand how they’re taxed and plan accordingly.

Strategy Tip: Timing is everything. Carefully plan when to exercise and sell your shares to optimize tax efficiency and leverage long-term capital gains.

9. Asset Location and Tax Loss Harvesting

Where you place your assets can make a big difference in your tax bill.

- Tax-Efficient Assets: These are best placed in taxable accounts.

- High-Growth Assets: These belong in tax-advantaged accounts, like Roth IRAs.

Tax loss harvesting involves selling investments at a loss to offset capital gains. You can use up to $3,000 in losses to offset ordinary income, with any excess carried forward to future years.

Strategy Tip: Regularly review your portfolio and harvest losses strategically to minimize your tax burden.

10. Non-Qualified Deferred Compensation Plan

This can be a great way to defer income to a future date, reducing your current taxable income.

Strategy Tip: If you’re in a high-income bracket and need additional tax deferral, consider utilizing a non-qualified deferred compensation plan.

11. Utilize a 529 Plan for College Expenses

529 plans are one of the best ways to save for college, thanks to their tax advantages.

- State-Specific Incentives: For example, Indiana offers a 20% tax credit on contributions up to $5,000. That’s a $1,000 credit for a $5,000 contribution.

- Federal Benefits: Earnings grow tax-free, and withdrawals for qualified education expenses are also tax-free.

Strategy Tip: Investigate your state’s specific plan and benefits to maximize your tax savings.

12. Don’t Forget Estate Planning

Estate planning is crucial for managing and reducing estate taxes and ensuring a smooth transfer of wealth.

- Gifting: Use the annual gift tax exclusion of $17,000 per recipient in 2024 to reduce the size of your estate.

- Trusts: Consider setting up trusts to manage and protect your assets.

- Education and Healthcare Expenses: Paying these directly for others can help you avoid using your lifetime gift exemption.

Strategy Tip: Work with an estate planning attorney to develop a strategy that fits your needs and ensures your legacy is protected.

By using these strategies, you can effectively manage your tax burden and grow your investments in 2024. As always, it’s wise to consult with a financial advisor or tax professional to tailor these strategies to your specific situation.

Investment advisory services are offered through Fusion Capital Management, an SEC registered investment advisor. The firm only transacts business in states where it is properly registered or is excluded or exempted from registration requirements. SEC registration is not an endorsement of the firm by the commission and does not mean that the advisor has attained a specific level of skill or ability. All investment strategies have the potential for profit or loss.